The $5 Trillion Pie: Healthcare's Fintech Opportunity

Executive Summary

Healthcare payments are one of the largest financial flows in the U.S. economy, about $4.9 trillion in 2023 (17.6% of GDP), or ~$14,570 per person. For perspective, that's roughly the same size as all US consumer credit card payments. That scale alone creates room for multiple category-defining platforms, especially as spend continues to compound. The opportunity is not just the top-line size, but the amount of manual workflows that can be modernized. It's estimated that health spend includes $900B of administrative cost, with up to 62% related to billing.

The market is structurally dysfunctional. Three features define it: excessive transaction costs, high denial rates, and high latency. We estimate 15-25% of a claim’s value is eaten up by transaction cost and 10% to 20% of in-network claims are denied (and higher for out-of-network), which drives expensive rework and write-offs. The claims filing process is very slow: it takes ~10-14 days to adjudicate and ~30 days to pay. In comparison, credit card latency is real time and the adjusted denial rate is under 3%.

Change drivers are finally aligned. (1) Clearinghouse consolidation has created near-universal connectivity and API access to payers, providing the infrastructure for the next generation of companies; (2) An accelerating AI arms race between providers and payers is driving adoption of next generation technology; and (3) Adoption of high deductible plans has created a growing cash pay healthcare market in the US. Going forward, we think clinical AI models will require new payment models, creating an opportunity to reshape the healthcare payment system.

Opportunity Areas We're Most Excited About:

- Solutions that decrease latency by providing real time adjudication. Credit cards introduced real time acceptance in 1973, and it is time for healthcare to modernize. We believe solving this problem will significantly reduce denials, increase transparency, and allow providers to collect patient responsibility at the site of care. Potential solutions include an exchange that sits between payers and providers (i.e. outsourcing adjudication), modern adjudication engines that sell into payers, or solutions that sit on top of existing clearinghouse infrastructure.

- Cash pay enablement solutions. As employers increasingly shift healthcare costs to members, we think new companies will emerge to enable the out of pocket consumer. Potential solutions include transparent marketplaces, embedded benefits/financing, and employer integration.

- New payment models for AI. CPT codes are time based and built for a human workforce. Clinical AI has infinite scalability, and therefore will require new payment models. The next generation of platforms will enable dynamic, usage-based, or outcome-linked pricing, supported by transparent verification of model performance.

Company Ventures' Fintech x Healthcare Portfolio Spotlight:

- Prosper AI builds AI voice agents that speak like humans, connect directly into practice management software, and handle tasks from patient scheduling and billing to insurance benefit verification and prior authorizations.

- Flychain is a financial operating system tailored for small and medium-sized healthcare providers, offering full-service accounting and bookkeeping, access to operating capital through upfront payment on insurance claims, and CFO-grade financial intelligence.

How To Engage With Terrarium:

- Build with us: join Terrarium as an entreprenuer in residence (EIR) to research, ideate, fund, and build your next company. Reach out to Yaniv directly at yaniv@companyventures.com to learn more.

- Already building in this space? Company Ventures’ early stage fund invests in pre-seed and seed stage digital health companies, check sizes $500k-1.5mm.

- Apply for our startup residency programs in NYC and Nashville. No rent and no equity working space for pre-seed and seed stage teams.

—

I. Why Change Is Accelerating: Economic, Consumer, and Technology Catalysts

We see 3 primary drivers of change in the US Healthcare financial system: (1) clearinghouse consolidation has created access to electronic payment rails, (2) Adoption of high deductible plans has pushed 80% of commercially insured members into de-facto cash pay arrangements, and (3) innovation in AI is automating manual payment flows and potentially clinical workflows in the future.

1. Clearinghouse Consolidation

Clearinghouse consolidation has reached critical mass, setting the stage for the next generation of innovation. Over the last 20 years, consolidation across healthcare clearing houses has allowed providers to connect to virtually every payer through API access. We believe this consolidation set the foundation for the modernization of the healthcare financial system, including real-time payments, automated denial prevention, and richer financial analytics. The top 5 clearinghouses in the U.S. account for well over 50% of total claim volume, with Change Healthcare alone representing about 40%, processing some 15 billion claims annually.1 As the referenced 2024 House Committee on Energy and Commerce review underscores, Change Healthcare is one of the largest health payment processors in the world, with its outage causing backlogs of unpaid claims and severe cash flow disruption to providers. The outage also created an opening for API-native competitors that are reimagining the clearinghouse model, such as Stedi, which positions itself as the leading API-first clearinghouse, delivering more efficient and modern infrastructure for claims processing.

2. The Emergence of the Cash Pay World

80% of commercial insurance members are living in a cash pay world. Among commercially insured individuals, the top 20% of members account for 83% of total spend.2 On average, patients in the top 20% of spending account for $21,338 per person and patients in the bottom 80% account for spending of only $1,251 per person. This means that each year 80% of commercial members, over 142 million people, will never reach the average deductible of $1,787 for single coverage3 and will primarily pay for their health insurance out of pocket. As a result of this, two distinct consumer segments have emerged in commercial: Cash Payers and Insurance Powers Users.

3. AI Innovation and Automation

A provider versus payer technology arms race is underway. Over the last 20 years, payers deployed new tech-enabled services for payment integrity (e.g., Cotiviti) and risk coding (e.g., Inovalon), while providers adopted revenue cycle management software (e.g., athenahealth and R1). A new generation of AI-enabled software is fueling rapid adoption across providers of new RCM tools. For example, SmarterDx leverages AI to capture missed revenue opportunities in coding and documentation, and Superdial and ProsperAI are using voice AI technology to automate denial management and phone eligibility checks. We believe that this arms race will continue for years to come, and will drive innovation cycles across healthcare stakeholders.

Clinical AI will require entirely new pricing and reimbursement models. Clinical AI renders obsolete reimbursement structures based on human scarcity. Current billing frameworks were created to compensate a human labor force and assume that a clinician’s time is the binding constraint. AI has the potential to deliver care at a significantly lower cost. As a result, we believe the current fee for service billing paradigm will change significantly over the next 10 years, creating an opportunity for new payment and insurance models.

Case Study: AI Therapy creates a New Payment Paradigm

Today, the average reimbursement for a 60 minute therapy session is $150 (CPT code 90837). A full-time therapist typically conducts 20 to 25 sessions per week, translating to an annual income of $150,000 to $187,500 based on a 50 week work year. In contrast to the traditional weekly therapy model, patients can engage with an AI therapy agent at any time, free from the constraints of scheduled, hour long sessions. This model is highly efficient and scalable, offering real time support and continuous engagement that can meaningfully improve clinical outcomes. Moreover, an AI agent can serve an unlimited number of patients with minimal incremental cost. As a result, we anticipate that AI therapy pricing will converge toward marginal cost, approximately $10 per month, and shift toward a cash pay model.

II. Breaking Down the $5 Trillion4

The U.S. healthcare financial system is enormous, processing $4.9 trillion in annual payments or $14,600 per person. It accounts for 17.6% of US GDP, and is projected to exceed an astounding $7 trillion by 2031. Health insurers process over five billion medical claims each year, highlighting the immense scale of the system.

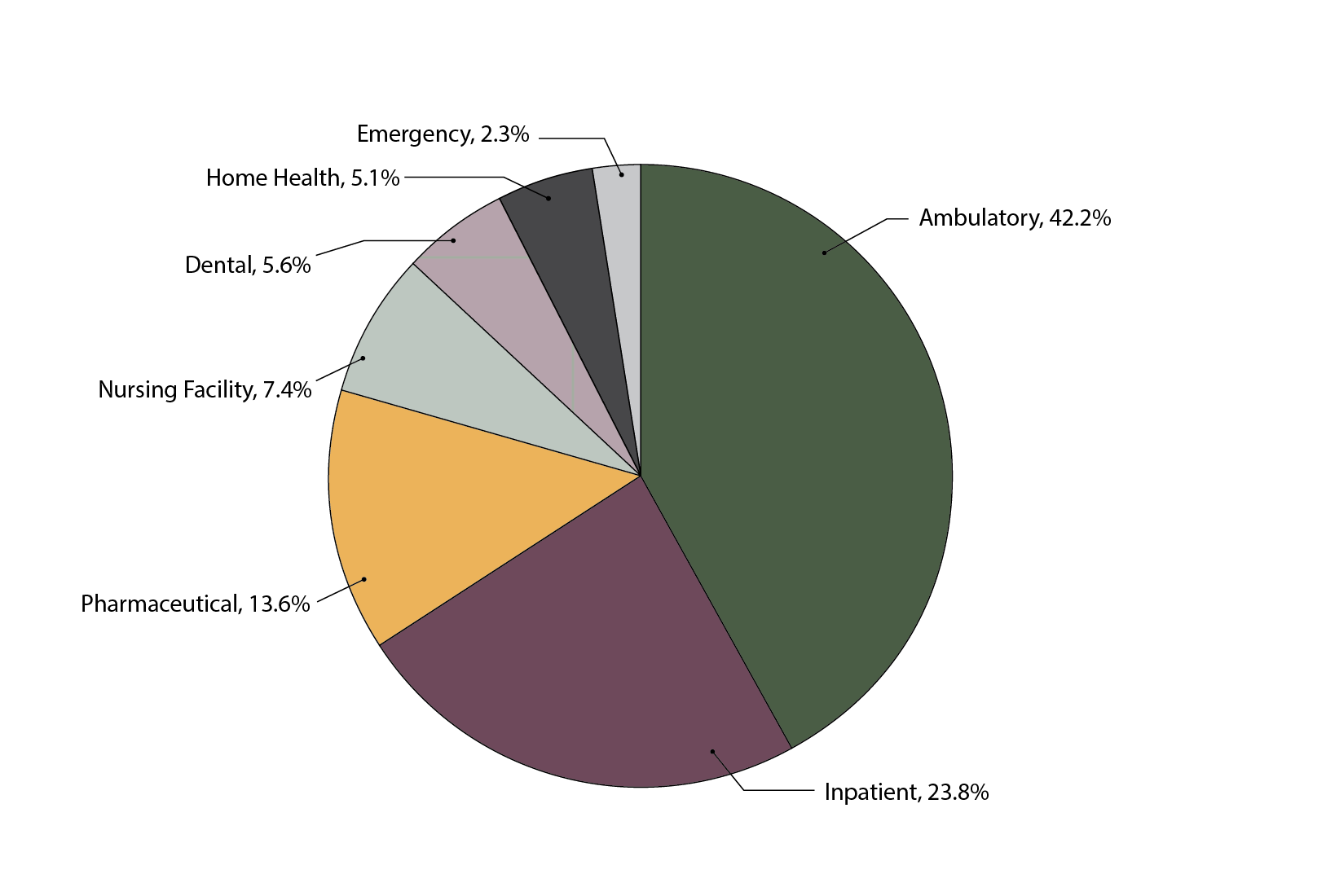

Where the money goes: 42% of spending flowed to outpatient and ambulatory care, or $1.03T. 24%, or $580B, to inpatient hospital services, and 14%, or $13.6B, to pharmaceuticals, with smaller shares for nursing facilities, dental, home health, and emergency departments.

Who pays: Private insurance (41%) and Medicare (30%) accounted for the majority of financing, while Medicaid (18%) and out-of-pocket payments (12%) filled in the rest. It's worth highlighting that 12% of out of pocket cash pay spend is $558B per year, or approximately $1,750 per American.

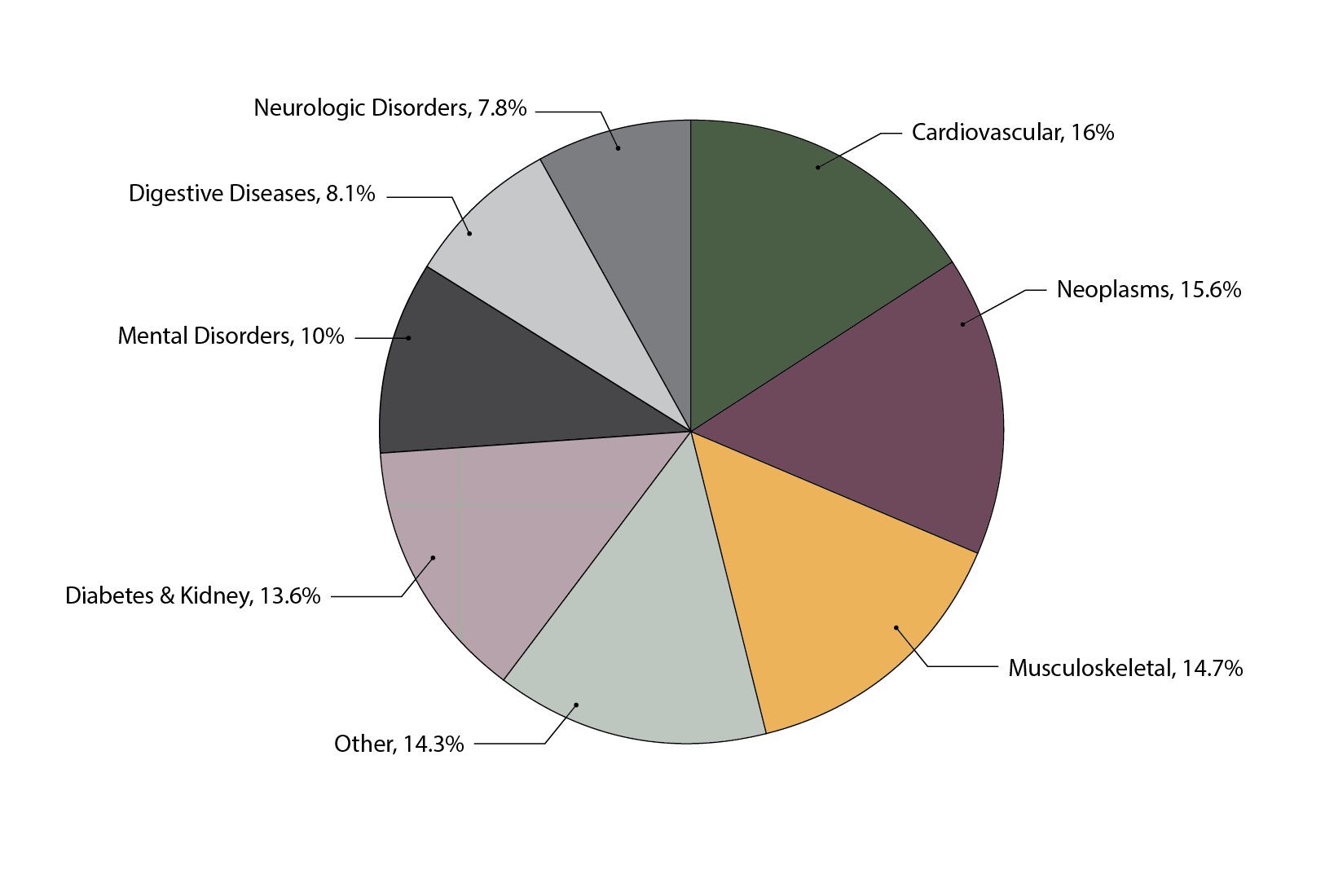

What therapeutic categories drive spending: Chronic conditions are the biggest cost drivers, led by cardiovascular diseases ($265B), neopalsms (i.e., cancerous and benign tumors, $259B), and musculoskeletal disorders ($245B).

Where it varies: Geography plays a huge role, with per capita spending ranging nearly fourfold, from $3,410 in Clark County, Idaho to $13,332 in Nassau County, New York, driven more by differences in utilization than price.

III. Comprehending the Dysfunctional Market

Despite being such a large market, there is near universal dissatisfaction across stakeholders in the US healthcare financial system. We believe 3 primary characteristics contribute to making the market dysfunctional: (1) excessive transaction costs, (2) high claim denial rates, and (3) high latency for payment.

1. High Transaction Costs

We estimate that 15% to 25% of a claim’s value is eaten by transaction costs. This figure includes the cost to verify insurance, time spent coding, RCM and clearinghouse fees, and lost revenue from denials. Of the $1 trillion in annual healthcare admin costs, estimates are that up to 62% are related to billing.5 Billing costs are disproportionately high in the US, where billing costs are 4x higher than in Canada. For comparison, credit card transaction fees are 1.5%-3.5% and institutional brokerage fees are 0.1%.

2. High Denial Rates6

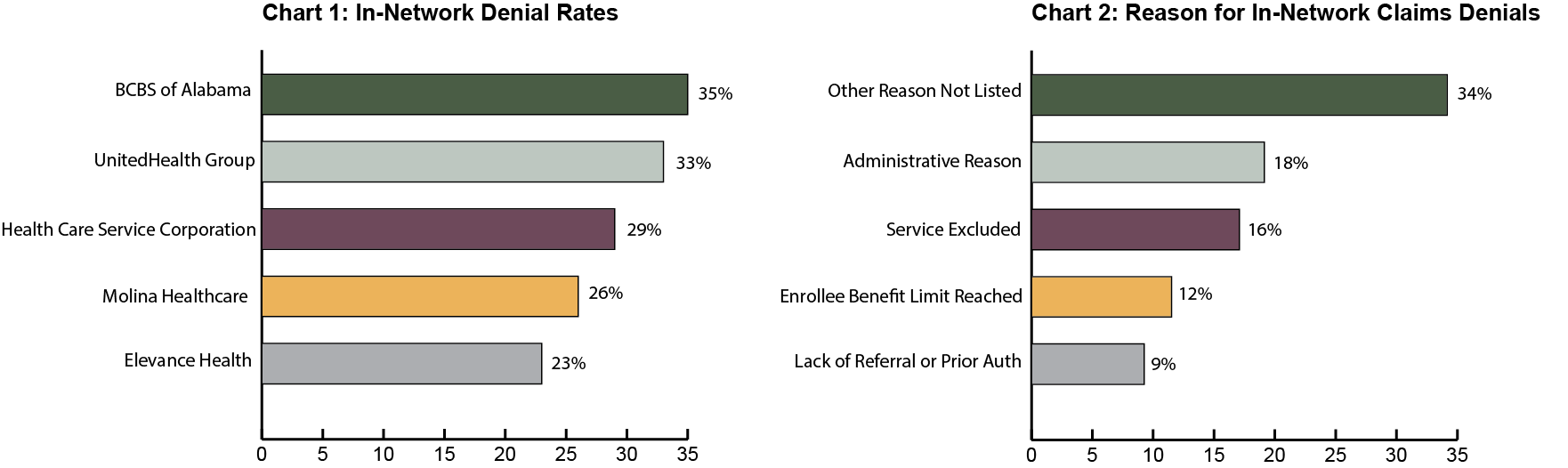

There are various studies analyzing US medical claim denial rates, and they all point to alarming high denial levels. KFF’s analysis of ACA (healthcare.gov) claims from the 2023 shows average in network denial rates of 19% across 392 million claims while out-of-network claims faced an even higher 37% denial rate. Similarly, Change Healthcare estimates that 12% of claims are denied, with up to 80% of the denials being avoidable. By comparison, U.S. credit and debit cards see denial rates of only about 6% (or less than 3% when you adjust for insufficient funds). Denials are especially costly because they trigger rework, appeals, and lost revenue that add up to tens of billions of dollars annually to the healthcare system.

3. High-Latency System: Slow Payments and Cash Flow Strain7

Processing claims is painfully slow. It takes ~10-14 days for health insurers to adjudicate a claim (i.e. confirm the amount of reimbursement) and 30 days on average for providers to receive payment (source). Latency is a major driver of denials and admin burden because providers cannot confirm cost and patient responsibility at the site of care. High latency is a unique characteristic of US healthcare, and most other industries have instant adjudication (credit cards, public equities, etc). On average, providers write off 7% to 10% of revenue from unpaid claims.

IV. Opportunity Areas

The next 10 years will mint category-defining fintech winners in healthcare. Enormous market scale plus adoption tailwinds make this moment exceptional. Here are three areas we’re most excited about:

1. Reducing Adjudication and Payment Latency

We believe that improving latency is one of the largest opportunities in the healthcare financial system. Solving this problem would reduce denials substantially, increase patient collections to nearly 100%, and reduce time to payment. Potential solutions could include creating a trusted intermediary between the payer and provider, building a tech enabled clearinghouse, or creating modern adjudication technology for payers.

2. Cash Pay Enablement

We see an opportunity to service the emerging cash pay healthcare market, which is 80%+ of commercial members each year. Historically, US consumers have been less willing to pay out of pocket for healthcare. But the emergence of the “optimizer” consumer is changing that, driving adoption for products like Superpower, Function Health, and Prenuvo. We are interested in solutions that create transparent, consumer-friendly marketplaces where patients can compare costs, access financing, and pay seamlessly. Employers, meanwhile, can integrate these solutions into benefits programs, enabling employees to tap into pre-tax dollars or installment options.

3. New Payment Models and Rails for AI

AI in healthcare is set to transform how value is priced and reimbursed. As clinical and administrative tools scale, from therapy chatbots to AI-powered dermatology diagnostics, they create an opening for new financial infrastructure. The next generation of platforms will enable dynamic, usage-based, or outcome-linked pricing, supported by transparent verification of model performance. We see a major opportunity for systems that serve as the financial clearing layer for healthcare AI, managing attribution, metering, and automated adjudication between payers, providers, and developers, ultimately aligning incentives around efficiency, accuracy, and access.

If you would like to engage further on this topic of Fintech x Healthcare, please reach out to yaniv@companyventures.com.

Citations:

- House Committee on Energy and Commerce. (2024). What we learned: Change Healthcare cyber attack. Retrieved from https://energycommerce.house.gov/posts/what-we-learned-change-healthcare-cyber-attack

- Dieleman, J. L., Beauchamp, M., Crosby, S. W., et al. (2025). Tracking U.S. health care spending by health condition and county. JAMA, 333(12), 1051–1061. https://jamanetwork.com/journals/jama/fullarticle/2823121

- Kaiser Family Foundation. (2024). 2024 employer health benefits survey. Retrieved from https://www.kff.org/health-costs/2024-employer-health-benefits-survey/

- Lo, J., Long, M., Wallace, R., Salaga, M., & Pestaina, K. (2023). Claims denials and appeals in ACA marketplace plans in 2023. Kaiser Family Foundation. Retrieved from https://www.kff.org/private-insurance/claims-denials-and-appeals-in-aca-marketplace-plans-in-2023/

- Sinsky, C., Colligan, L., Li, L., Prgomet, M., Reynolds, S., Goeders, L., Westbrook, J., Tutty, M., & Blike, G. (2016). Allocation of physician time in ambulatory practice: A time and motion study in 4 specialties. JAMA, 315(7), 758–766. https://jamanetwork.com/journals/jama/fullarticle/2673148

- MD Clarity. (n.d.). Average days to collect payment (RCM metrics). Retrieved from https://www.mdclarity.com/rcm-metrics/average-days-to-collect-payment

- Journal of Managed Care & Specialty Pharmacy article. (2021). Retrieved from https://www.jmcp.org/doi/10.18553/jmcp.2021.21252